The future of communications

Global communications are changing. With data demand growing faster than ever before, how does satellite technology offer the opportunity to change how we connect?

Electronic communications have a long history, stretching from when the first telegraph sent clock signals the length of a garden in the 1800s. The network grew rapidly from that point, linking first neighborhoods, then cities, and – 157 years ago – the first subsea cable enabled rapid communications between continents. Subsequent technology has since changed beyond all recognition in some respects, with optical cables replacing copper telegraph wires and delivering data speeds and capacities unimaginable to our predecessors. But in other ways it has stayed the same – an ever-expanding web of land-based and underwater cables linking centers of population across the globe.

So where do satellite networks fit into this essentially earthbound picture? Well, that’s one of the most exciting areas of growth in the communications industry at the moment. Fixed infrastructure such as undersea cables is costly to deploy, only connects a limited number of locations and has a capacity restricted by the number of fibers in the cable. Some remote communities will never have fiber because the internet providers will never get ROI on such a big infrastructure project for a relatively small population. Meanwhile, recent developments in satellite technology have slashed the cost of putting capacity into orbit, making satellite networks far more competitive and opening the door to truly global, high bandwidth coverage.

To put the demand for data into perspective, it’s helpful to look at how it has increased in the last five years. In 2017, global consumer IP data totaled 1.2 zettabytes. In 2021 we hit 3.2 zettabytes, and in 2022 are projected to use nearly 4 zettabytes. These are unimaginable numbers: a zettabyte is a trillion gigabytes, or the equivalent of 350 billion DVDs. To put it another way, since the internet was born in 1983, it took 34 years to use one, single zettabyte of data. We now use over three times that in a single year.

It’s this demand that is driving infrastructure, both on land and in the sky. Multiple sources contribute to the need for so-called ‘big data’, including manufacturing, government, IoT, healthcare, media and entertainment. The importance of connectivity has also shifted – while in the past, users might view an internet outage with resignation, online access is now essential for a host of business and personal applications. The recent coronavirus pandemic only exacerbated this, with many people at home, depending on VPN connection and video conferencing to be able to work not only effectively but at all! It also massively boosted personal device use – a survey in April 2020 showed that 76% of users aged between 16 and 54 were spending more time using their smartphones than previously. The number of connected devices has also skyrocketed, from 12.5 billion in 2010 to 50 billion in 2020.

Maritime Satcoms is seeing similar growth. In 2021, there are 37,334 vessels using VSAT to connect, nearly 10,000 more than in 2018. By 2029, there is expected to be over 79,000 vessels connecting. Taking a holistic view of the land and maritime markets, we have a potentially major problem in front of us – the insatiable demand for connectivity and data is increasing exponentially, yet growth of capacity is actually slowing down, driven by the time involved in laying cables and new environmental concerns. If nothing changes, demand will outstrip capacity by around 2028 – that’s terrifyingly soon.

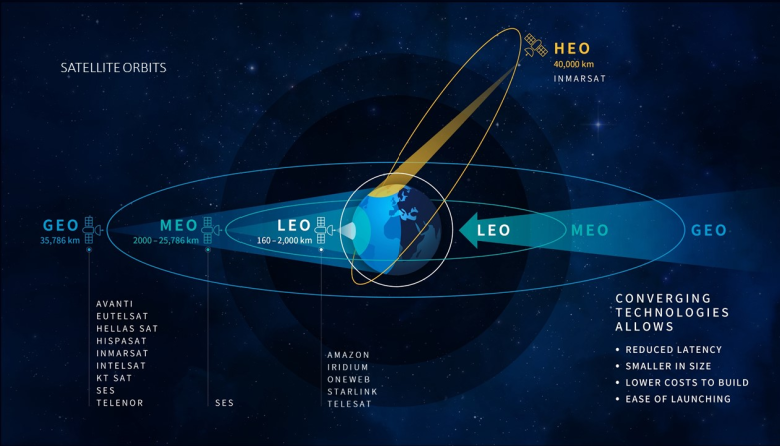

This looming deadline is a driver behing the more recent increase in the new and increasing number of satellite launches. Inmarsat has already added significant capacity to its geostationary (GEO) network and is continuing to do so with multiple new satellites, including a pair launching into HEO (highly elliptical orbit) to cover the North Pole. SES are deploying their new, extremely powerful mPower network in medium earth (MEO) orbit, providing extensive, multi-gigabit, low-latency coverage to 96% of the global population with just six satellites. Meanwhile Amazon, Iridium, OneWeb, Starlink and Telesat are all focused on services in low earth (LEO) orbit, with their proximity to Earth delivering the lowest latency of all, at the expense of needing multiple satellites to deliver seamless coverage.

This proliferation of networks has been made possible by the convergence of multiple technologies, notably the development of reusable launch vehicles. As a result, launches have become far more economic: in 1981, the cost of launching a payload into space using the space shuttle was $55,400 per kilogram carried. By comparison, today, the Falcon craft developed by SpaceX have reduced that to $951 per kilogram. In addition, low orbit satellites are smaller and cheaper to build. As a result, satellite communications are now a cost-effective option compared with land-based infrastructure and are expected to start to pick up data traffic previously carried exclusively via the terrestrial fibre network, such as cellular backhaul.

For the user, these changes bring multiple potential benefits. Lower orbit networks allow latency-sensitive data such as gaming and hi-definition, reliable video calls to be carried over satellite. They are also global when sufficient satellites are deployed, with the ability to serve anywhere on Earth with the same high-speed data. According to Statista, in 2021 global internet penetration rate is still only 59.5% - that’s a staggering 3,160,000,000 people unconnected and satellite communications is going to help resolve that. In addition to the life changing impact getting online makes to people and businesses, there’s the huge growth in Industrial Internet of Things (IIoT) which in remote areas will also rely on satellites, as well as cellular back-haul and providing secure communications for everything from blue light services to embassies should terrestrial networks be insufficient.

For shipping, this has ramifications for business at sea, GMDSS, collateral tracking, logistics, cyber security, sustainability and crew welfare. And with multiple providers competing, economic logic suggests that the cost of data will reduce, just as we saw with the growth of cellular networks.

Of course, with a wide range of networks using multiple orbits and bands, one area the customer needs to box clever is in choosing their terminal equipment. Satellite technology is an investment, and if a new antenna is needed to access each network, or change bands, there will doubtless be reluctance to change. That’s why at Intellian, as pioneers, we made an early decision to be first in the world and future proof our antenna for our customers: with our NX series, you can access GEO, MEO, LEO and HEO orbits, and switch between Ku- and Ka-bands with a simple conversion kit, all from the same innovative platform so you’re not locked into one provider. With Intellian, you have choice!

The future is diverse and exciting, and we’re ready for it.